Abstract: Based on the current domestic and international economic development and market supply and demand, this paper analyzes and predicts the price trend of raw and auxiliary materials for foundry and discusses the development of China's foundry industry. The aim is to grasp the market conditions, adjust the production structure in time, respond to market changes, reduce material costs, and create greater and more direct economic benefits.

The foundry industry is an industry that consumes a lot of energy and mineral resources. It not only consumes a wide variety of materials, but also a large number. According to statistics, in 2007, China's casting production has exceeded 30 million tons. According to the empirical formula, the annual demand for metal materials is about 37.5 million tons, the modeling materials are 33 million tons, various refractory materials are 10.8 million tons, and other various auxiliary materials are 11.25 million tons. A variety of casting raw and auxiliary materials of 92.55 million tons. At present, the contradiction between China's national economic development and energy resources is increasingly prominent. Therefore, the awareness of resource conservation and emission reduction in the industry is established. High-quality casting raw and auxiliary materials are selected to reduce material consumption and establish a conservation-oriented society. Contribution is very necessary. In recent years, the world economy has generally maintained rapid growth. At the same time, the economies of developed and developing countries have been declining. The regional pattern of world economic growth has changed. Many accumulated problems and contradictions have become increasingly apparent, especially the global economic imbalance. Market relations are getting tighter, economic risks are increasing, and uncertainties are increasing. Economic growth is the driving force of social development, but China, which is in the midst of rapid economic growth and social transformation, is also experiencing a series of tests of social problems and changes in concepts. In this context, the prices of raw materials for casting are also greatly affected. In order to improve the economic efficiency of enterprises, the quality of materials and the high and low prices are crucial.

[ International Economic Environment Development and Impact ]

The world economy continues to maintain steady and rapid growth, and it also provides good external conditions for China's economic development. Such as: continue to expand exports, further expand imports, so that import and export trade maintains a stable and balanced development; optimize trade structure, increase exports of high value-added products and vigorously introduce advanced technology and equipment; the slowdown of the world economy will also help prevent the domestic economy from being hot Wait. At the same time, it will drive the development of the foundry industry and increase the close attention to the raw and auxiliary materials for casting.

China's sustained and rapid economic development is an important force supporting the growth of the world economy. In 2007, it contributed to the world's economic growth. The current international economic environment has also created greater challenges and pressures on the prices of China's foundry materials. for:

1) International oil and food prices continue to fluctuate at a high level, which has created a large input inflationary pressure on China.

2) The pressure for RMB appreciation continues to be large. As a result, the input inflationary pressures have increased, the trade imbalance has become more serious, and the adjustment effect of monetary policy on credit and investment scale has been weakened.

3) The trade surplus continued to expand, and trade protectionism against China further intensified. According to the statistics of the US Department of Commerce, China’s trade surplus with the United States from January to November in 2007 was 237.5 billion U.S. dollars, an increase of 11.1% year-on-year. According to statistics from the Eurostat, China’s trade surplus with the EU in January-October 2007 was 132.2 billion euros, an increase of 26.1% year-on-year.

4) The United States, the United Kingdom, and Canada are in a rate cut cycle. The European Central Bank also suspends interest rate hikes, while China is raising interest rates, and the market is expecting more interest rate hikes in China. Coupled with the expectation of continued appreciation of the renminbi, international speculative capital may be possible for China. Will have a big impact.

In such a world economic environment, China's macro-control policies will continue in 2008. For various reasons, the prices of raw and auxiliary materials will also fluctuate greatly, and the growth trend is not expected to change.

The influence of national macro-control and the analysis of price trends of some materials

First, non-ferrous metals

1) Review 07 market, forecast 08 trend

In 2007, China's non-ferrous metal industry was in a high boom cycle. The market consumption growth is huge, which is not only supported by the strong consumption growth under China's high-speed economic growth rate, but also thanks to the regulation of China's relevant industrial policies to promote industry integration. However, the non-renewable and scarce acceleration of non-ferrous metal resources has driven the Chinese non-ferrous metal market to concentrate and integrate.

After the sharp increase in prices of copper, aluminum and zinc in 2006, the price of lead-tin-nickel in 2007 also increased significantly. What followed was that the sector index rose by as much as 390%, far exceeding the Shanghai and Shenzhen 300 Index. On the one hand, the supply-demand relationship has not been fundamentally reversed. On the other hand, as the value of resource commodities has gradually gained investment recognition and the situation of global inflation has become more serious, the overall trend of non-ferrous metal products in 2007 has maintained an upward trend.

From the demand side, China's strong economic growth has further stimulated the "China factor" to promote prices. Recently, the price of basic metals in LME has rebounded. The market expects to shift from worrying about insufficient demand to worrying about supply shortage. In addition, the continued weakening of the US dollar and rising energy prices are also important factors in the recovery of non-ferrous metals prices.

From the perspective of supply, the increase in global mining capital investment indicates a optimistic expectation for the industry's business cycle. But as developing countries become the main growth point of global consumption, it is still to be seen whether there will be a decline in future consumption.

We believe that the supply and demand of non-ferrous metals in 2008 tends to be elastic and tense. Combining inventory has not yet emerged from historical lows, and resource commodities have gradually gained investment recognition, and it can be predicted that the economic factors of the non-ferrous metals industry have not disappeared.

2) List some material analysis

1. Electrolytic copper

The copper industry is an important industry in the national economy. Among the 124 industries in China, 113 industries use copper products, accounting for 91%. The copper industry is also highly correlated with other industries. China's copper consumption last year is expected to account for a quarter of global copper consumption, and the increase is significant. In terms of copper prices, China's copper prices have been constrained by various factors in recent years. In the long run, copper prices are represented by consumer demand represented by China and India's economic growth, and are confronted with abundant production of natural copper resources and mining and smelting technology. Since the development prospects of both supply and demand are very good, copper prices do not have the support of a long-term fundamental as well as oil prices. At the same time, there is a time lag due to the balance between demand and supply, and there are more links between macro supply and demand and terminal supply and demand.

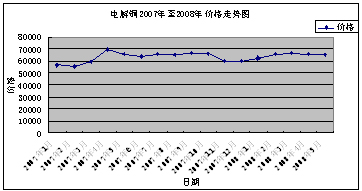

At the same time, as shown in Figure 1, the price of electrolytic copper reached the highest level of 69,380 yuan / ton in April 2007, the lowest price was 55,590 yuan / ton in February, the difference was 13,790 yuan / ton, during the period from January to May 2008, although the price was higher than 07 The year has increased, but the price is basically stable. Therefore, it is predicted that the price of electrolytic copper will rise steadily in the second half of 2008, and there will be no ups and downs in case of special circumstances and artificial speculation.

Figure 1 Price chart of electrolytic copper from 2007 to May 2008

Next page

CNC Stainless Steel Parts,Stainless Steel Parts,CNC Machining Parts,aerospace industry,Boats accessories

Chongqing Henghui Precision Mold Co., Ltd , https://www.citool.com